Interest rates used in project evaluation should command the attention of anyone interested in water projects. The lower (or higher) the interest rate used in project evaluation, the more (less) likely a given project will be judged economically viable. The interest rate issue should NOT be viewed as an issue in the exclusive domain of economists and financiers. Otherwise, project evaluation will be co-opted by “off-line” discussions among economists and financiers selecting the interest rate.

There are two ways to think about interest rates for project evaluation: (i) policy, or (ii) financing:

- “Policy” interest rates are found in handbooks for project evaluations used by federal and state agencies to assess financial feasibility generally for the purpose of public funding.

- “Financing” interest rates pertain to terms for project financing from the capital market.

Jason Bass, Featured WSC Blogger is preparing a series of posts on policy interest rates. In this post, I discuss financing interest rates.

The Importance of Interest Rates

Water projects are classic investment opportunities. Projects involve investment of significant resources up front over a period of years. The benefits (or returns) are in the “out years” not starting until after project completion. Are the benefits in the “out years” sufficiently large to offset the costs incurred during the project development period?

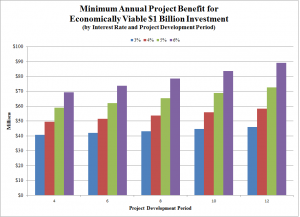

Consider a stylized example. Suppose a $1 billion capital project has four years of project development costing $250 million each year. Post-project completion, the project generates anticipated annual benefits of $30 million for 50 years. Does 50 years of annual benefits of $30 million ($1.5 billion) justify a $1 billion investment? Not necessarily. We need to account for the timing of costs and benefits. The interest rate measures the time value of money. The question is how does the value of the schedule of costs incurred during project development compare to the value of the schedule of annual benefits enjoyed post-project completion?

Economists answer this question with by comparing the present value of costs with the present value of benefits. (Present value uses the interest rate to value the timing of project costs and project benefits.) For the 4-year, $1 billion project discussed above, the smallest annual benefit for the present value of benefits to equal $1 billion ranges from $41 million at an 3% interest rate to $69 million at an 6% interest rate (see chart below). Therefore, with an annual benefit of only $30 million, the project in the stylized example is not economically viable (present value of project costs exceed present value of project benefits). Note that the longer the project development period, the higher the smallest annual benefit for a viable project for a given interest rate

Conceptual Components of Interest Rates

At the time of project evaluation, the choice of interest rate involves judgment calls. There are two aspects: (i) market reception and (ii) future versus current market conditions:

- market reception: under what terms would the capital market finance project investment today?

- future versus current market conditions: given that project financing will not occur immediately, how will conditions at the time of financing compare to conditions today?

A conceptual framework is useful to guide discussion. See framework below for one commonly used in economics and finance. The interest rate for a project equals the return on a benchmark security plus a risk premium. A common benchmark is a “risk-free” security such as yield on 10-Year U.S. Treasury Notes. The “Risk Premium” is the extra return needed to finance the project given financial risks borne by capital providers.

|

Interest Rate |

= Benchmark Return + Risk Premium |

| = Yield on 10-Year Treasury Notes + Risk Premium |

For an assessment of current market conditions, the yield on 10-Year Treasury Notes is a “look-up” exercise.

Especially when thinking about future market conditions, it is useful to breakdown the yield on 10-Year Treasury Notes into two components: real interest rate (return adjusted for inflation) and expected inflation.

|

Yield on 10-Year Treasury Notes |

= Real Interest Rate + Expected Inflation |

Since 2003, the U.S. government has issued Treasury Inflation Protected Securities (“TIPS”) that adjusts principal payments by inflation. Therefore, the yield on TIPS provides a market estimate of the real interest rate. Using the above equation, one can infer a market estimate of expected inflation by comparing yields on 10-Year Treasury Notes with TIPS yields.

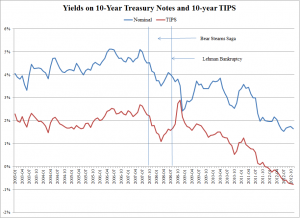

Treasury Yields and TIPS Yields

The chart below shows monthly data on Treasury Notes and TIPS yields (source: Federal Reserve Board). Until late 2007, the yield on 10-Year Treasury Notes fluctuated between 4% and 5% and TIPS yields fluctuated around 2%. The problems at the Investment Bank Bear Stearns (the first fire-drill of the financial crisis) became public in late 2007 and the Lehman Bankruptcy (the penultimate fire-drill of the financial crisis) happened in September 2008. Treasury and TIPS yields went into free-fall during these financial crises and later with other crises, such as Europe. By November 2012 (later monthly data not yet available from Federal Reserve Board at time of this posting), the yield on 10-Year Treasury Notes has fallen below 2% and TIPS yields have become negative (more on this below).

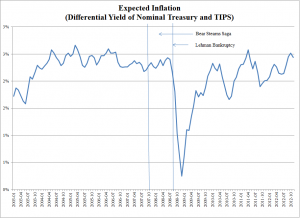

Expected Inflation

In contrast to treasury yields, the market’s estimate of expected inflation has been more stable (see chart below). Pre-financial crisis, expected inflation hovered around 2.5%. It remained stable through the Bear Stearns crisis. With the Lehman Bankruptcy, expected inflation fell steeply during the rest of 2008 and for six months into the first Obama Administration. By the start of 2010, expected inflation returned to its pre-financial crisis levels, fluctuating between 2% and 3%.

Implications for Project Evaluation

An interest rate based on today’s market conditions is probably too low for evaluations of long-term projects. Based on the above data, I conclude that today’s treasury yields below 2% reflect historically low, and in fact, currently negative real rates. With expected inflation returning to pre-financial crisis levels, using an interest rate reflecting today’s conditions is a bet that real interest rates will be negative long-term. In my opinion, this is not a good bet.

In the mid-1970s, I was a research analyst at the RAND Corporation examining international capital market conditions for the Council of International Economic Policy at the White House. (This group was later disbanded as a result of a follow-on study on international wheat agreements, but I digress.) The mid-1970s was a time of severe concerns about international capital market dislocations created by OPEC oil price increases. The RAND study noted that during this time period, real interest rates were negative. Therefore, despite policy concerns about an international capital shortage, capital was cheap (not dear). The Ford Administration jettisoned plans to solve a “non-problem.”

We at RAND were struck by the fact that, during financial crises, the “flight to safety” by foreign buying of US treasury notes and bonds meant that the market was “buying safety in America” by accepting negative real rates. Later in the 1970s when that financial crisis was in the rear view mirror, real interest rates rebounded to their long-term historical levels of 2% to 3%.

Takeaway

What does experiences from 40 years ago have to do with project evaluation today? The interest rate used for evaluation of a long-term project should use an interest rate of 4.5% plus a risk premium. The real rate will return to historical levels long-term. When? (If I knew I would trade interest rate futures.) Using the experience of the 1970s as a guide, negative real rates will last at most only a few years. An 2.5% expected inflation is consistent with (i) yield differentials between nominal 10-year Treasury Notes and TIPS and (ii) long-term inflation in the United States since the 1980s.

| Interest Rate |

= Real Rate (2%) + Expected Inflation (2.5%) + Risk Premium (?) |

What about the risk premium? See my next post in this series on January 18th.

I applaud that you make so clear a distinction between the selection of a discount rate for evaluating feasibility in a policy context as compared to a financing context. The distinction is frequently overlooked even at the highest levels of corporate and public decision-making. The result, all too often, is resource allocation that does not achieve objectives, results in decision paralysis and/or leads to legal entanglement. In my experience the error works mostly in one direction; it is usually the adoption of a market financing perspective in the assessment of projects whose primary objective is not simply profit maximization but perhaps, for example, equitable distribution, improved human health, inter-regional cooperation, or cultural preservation. This has been the mistake of the Federal Government’s Office of Management and Budget (OMB), which through its directives stipulates the use of capital market yields as the basis for discount rates in benefit-cost analysis of projects potentially funded with Federal dollars. All too often the OMB approach completely misses the mark on the objectives of the project under consideration or the context of the analysis. An important case of the latter, which I will be discussing in the coming weeks, is cost-benefit analysis in the quantification of Native American Indian Federal Reserved Water Rights.

Pingback: Proposed Down Payment for Financing the Texas Water Plan | Water Strategist Community Blog