Hydrowonk’s Take on the BDCP

Time to step back and collect the key points of this 8-post series on the Bay Delta Conservation Plan. There were many themes relevant to the BDCP or, for that matter, any other water project. By following them, one can have an accurate assessment of the economics, risks and choices related to a venture. Ignoring them will be a recipe for disappointment if not outright failure.

Before discussing the lessons, I want to discuss some questions I have received “off-line”:

Here goes. Rather than turning this into a sea of links to past posts, I organize the discussion around the “key takeaways” of each post. Perseverance is required. I end with predictions in the conclusion (no peeking!).

Post 1: Project Capital and Investment Costs

Get a finance plan at the start of a project. Otherwise, you have an incomplete picture of the full capital investment. In the case of the BDCP, the economic costs of debt service reserves and working capital can total $500 million to $750 million. With underwriting fees, the full price tag can total $1 billion. Not a small estimation error.

Estimate capital costs for the time the project is built. The current practice of securing an “opinion of probable cost” based on what the project will cost today is only the first step. Market trends in goods and services must be assessed to convert estimated costs today into estimated cost in future years when construction actually occurs. Especially when projects start years out and have long construction periods, the “early” cost estimates will predictably be below actual costs. For the BDCP, this may be a $1.4 billion issue.

DWR has done neither. A multi-billion project will cost at least $2.4 billion more.

Post 2: Cost of BDCP Water–Project Timing and Risks

Timing matters. The BDCP is a project where billions of capital commitments are made at the start, followed by at least a decade construction period. Then deliveries start. Failure to take into account timing of commitments versus start of deliveries and the related risks severely understates the “cost of water” from a proposed project.

The BDCP materials are lacking on these matters. The calculation of annualized cost of water ignores the decade delay in the start of deliveries and assumes no risk other than hydrology. In that estimated deliveries are the result of computer modeling, is the project accurately viewed as (other than hydrology) “risk free”?

Hydrowonk’s intuition says no. Where the BDCP pitches the cost of water between $300/AF and $400/AF (inflation-adjusted), a more reasonable range is $625/AF to $890/AF (inflation adjusted). The BDCP project needs a full risk assessment. While there is none to date, my experience with capital markets suggests that the market will demand a risk assessment before financing.

Speaking of financing, the absence of a finance plan prevents one from estimating the project’s cost of water. What will be the needed debt coverage requirement for the project? The capital market today looks at debt coverage in issuers finance plans and their ability to meet them in addition to the debt coverage obligation stated in offering statements. The BDCP material is silent about the former. The project’s debt service requirements can easily put the annual cost of BDCP water above $1,000/AF (inflation adjusted). Without a finance plan, it is impossible to assess the economic cost of debt service coverage.

Post 3: State Bond Funding

Reliance on future state bond funding is becoming more speculative. In California, state indebtedness has exploded. The amount of debt outstanding has doubled since the last successful water bond issue. For the state water bonds passed since the 1980s (cited in BDCP materials), voter support for water bonds falls with increases in the debt burden (state debt outstanding plus size of bond relative to personal income). Given the size of existing debt and the 2014 water bond, the expected vote share in favor is only 42.4% with only a 12.2% probability of passage. The Vegas odds would be 7-1 against passage.

The “headwinds” against state bonds has significant implications for the BDCP. The BDCP calls for $7.93 billion in state bond funding of environmental programs. Assuming that these projects are an integral part of the “political package”, what is Plan B if the 2014 water bond fails? Even if the first stage of environmental funding is secured ($1.514 billion), the BDCP contemplates a “second water bond” in the future to fund $1.9 billion in environmental projects. If California’s debt burden continues to grow, this second stage environmental funding will be facing even greater headwinds.

While for different reasons, environmental interests and water users should care about the “credibility” of bond funding. For environmentalists, will a BDCP look like the QSA (let water user projects go ahead with the promise of achieving environmental aims, Salton Sea restoration, in the future). For water users, if the BDCP lacks funding to achieve defined environmental goals, will regulations be “re-opened” (legally or politically) that drive down water yields.

The California Legislature recently ended its sessions with serious discussions about a smaller water bond. Based on the historic record of support for water bonds and debt burden, a smaller water bond will do better in the 2014 election, but not much. A $2 billion water bond has an expected vote share of 46.4%, with the probability of passage only 27.4%.

The takeaway here is that a successful water bond will need a significant effort for success. Leadership will be critical. Put together a program that extends beyond the BDCP and yields a broad-based package to avoid the type of conflicts within the water community experienced a generation ago with the Peripheral Canal.

Post 4: Water Supply Reliability

DWR estimates that the BDCP will have an annual yield, on average, between 1.2 million AF (under the high Delta Outflow Scenario) and 1.7 million AF (under the low Delta outflow scenario). The extra water occurs in normal and wet years. Without storage, BDCP water is simply a junior priority water source.

The BDCP avoids a further loss of project water supply, not an increase in water supplies. It uses existing storage in the state and federal projects to increase supplies in dry and critical years. The BDCP does not reduce the greatest projected water shortages in California. It does trim the size of shortages occurring in less severe conditions.

Unfortunately, DWR does not share much of its extensive analysis of the risk and size of water shortages. What is the time profile of the probability of water shortages? The implied annual probability may be in the range of 40% to 70%. That is, DWR projects regular water shortages even with the BDCP. If so, is there a “new normal” in California? Is projected growth in California viable?

An important takeaway is that the BDCP is not a solution to California’s water supply reliability challenge. Additional storage is the missing ingredient. The BDCP is not a cure all. After all, the BDCP is only trying to secure a take permit from state and federal resource agencies.

Post 5: Will There Be Buyers for BDCP water?

The DWR narrative on the BDCP water supply is a case of severe oversell. DWR understates capital costs. DWR’s calculation of the cost of BDCP water ignores the difference between timing of capital commitments (2015) and the start of deliveries a decade later. BDCP water is demonstrably inferior to stated alternatives: non-firm supplies versus reliable water supplies, untreated versus treated water, location (Northern California versus already at water user’s system), and project risks (computer modeling versus operational experience).

Time to see who signs up and make contractual commitments to the BDCP. Make the BDCP a supplemental project to existing state and federal projects. Apportion share of project yields and project costs. Allow trading in BDCP project units. None of this is new. The original SWP project follows these principles. So does the federal Big Thompson Project in Colorado. Does this dog hunt?

Voluntary decision-making could cascade through the structure of California water agencies. Contractual commitments from member agencies of SWP contractors should back the commitment of SWP contractors. Member agencies, in turn, should secure contractual commitments from their member agencies.

The BDCP is a generational project. Contractual commitments secured through an open and transparent subscription process will avoid the inevitable second guessing that accompanies any water project.

Post 6: What About Those $5 billion Net Benefits?

The most convincing analysis and information provided by DWR is the discussion of the economic losses from water shortages. The annual economic cost of municipal water shortages top $1,000/AF (inflation-adjusted) for 10% shortages and approach $2,000/AF (inflation-adjusted) for 20% shortages. The annual economic cost of agricultural water shortages is an order of magnitude smaller. This difference will become the source of pressure in cost allocation discussions. Unless municipal water users fund significant subsidies, the BDCP must become a supplemental water project for municipal water users.

The entire venture may be underwater (see table). If DWR failed to adjust for the timing of water deliveries relative to cost (as they did in its calculation of the cost of BDCP water), DWR overstates the present value of project benefits by about one-third. As discussed above, DWR understates capital costs and, therefore, understates costs by about 15%. With these adjustments, the BDCP is underwater.

Post 7: Statewide Economic Impact

BDCP impact on statewide income equals about one month of trend growth. More than 90% of the income impact is from avoided water shortages.

The stated job creation from the BDCP is severely overstated. The estimated 1.1 million full-time equivalent jobs counts jobs lasting multiple years multiple times. Actual full-time job creation is about 25,000 full-time equivalent jobs per year. Avoiding water shortages is the job creator. Like statewide income, the job-impact of the BDCP equals about one-month of trend growth in state employment.

The BDCP’s economic merits are from reducing water shortages. The BDCP is not a general economic stimulus program.

Post 8: What is the Baseline for a California Without Tunnels?

I am not aware of any consensus. I have heard a diversity of viewpoints in off-line discussions. None argue that the no tunnel scenario would yield less water than projected by DWR. All argue that there will be significantly more water than projected by DWR. If this proves the case, the annual cost of BDCP water will easily exceed $1,000/AF (inflation adjusted).

What Does All This Mean for the BDCP?

Nothing is good or bad save the alternatives make it so. The BDCP is costly. There are significant project risks. As with any water project, the economics of water supply and reliability drive answers.

If not the BDCP, then what? For the state and federal projects, there are two components to water supply reliability: volume of water from junior water rights and storage. The BDCP has focused on the first component—investments to protect the existing yield of state and federal projects.

How do investments in storage stack up? There are north and south of the Delta storage alternatives. How does the investment of a few billion in storage compare with the investment of $15 billion on BDCP water conveyance facilities? Without this comparison, one does not know whether the BDCP is a good or bad idea.

The BDCP narrative started with discussion of better risk management. It was surprising, therefore, that earthquake risk become a bit-part player by the time DWR’s economic analysis was released. As I think about California’s future, I am surprised that the risk and consequences of levee failure in the Delta hasn’t received more attention.

BDCP’s Future

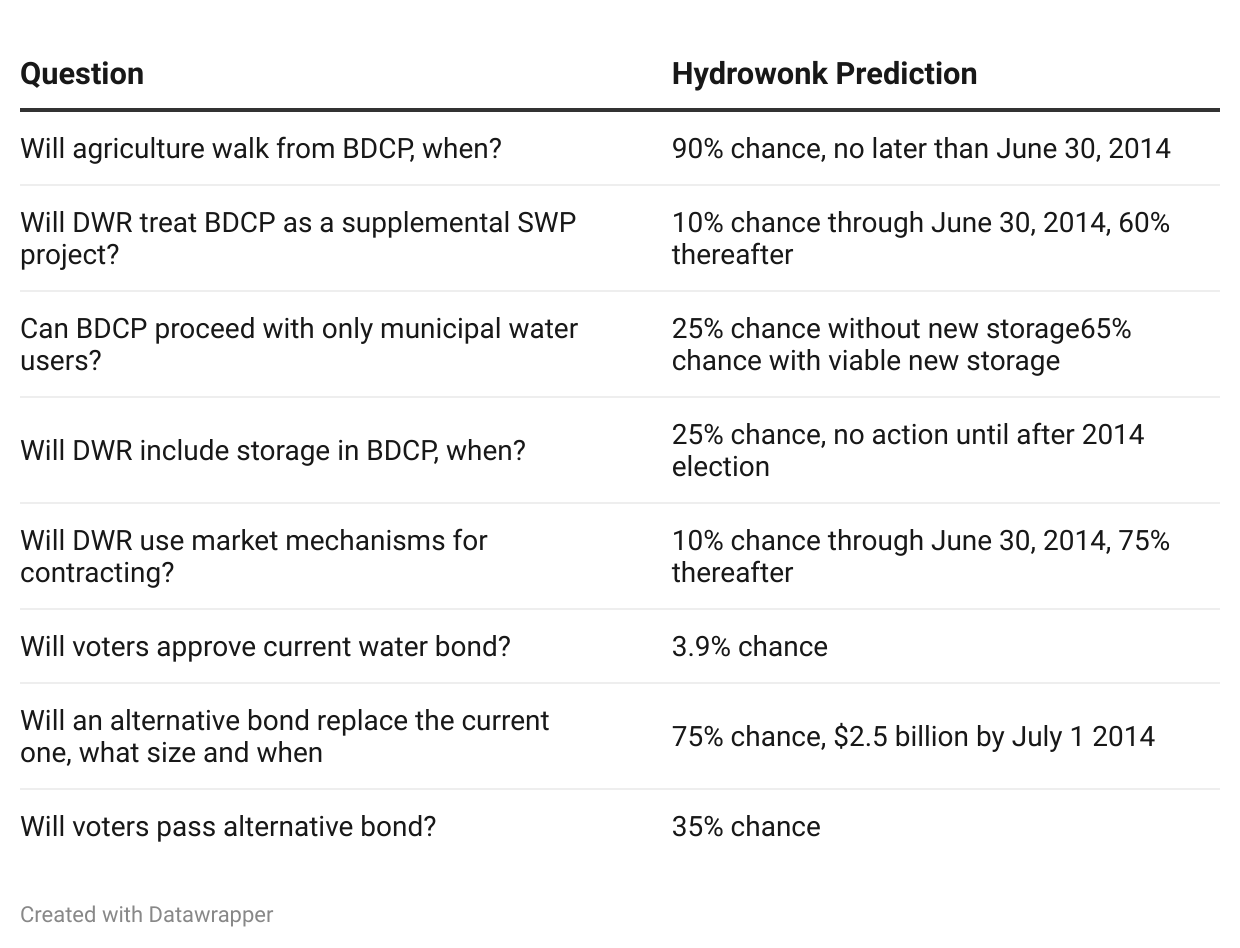

I finish this series with predictions about the future—always a tricky business. I have been wrong before and will undoubtedly be wrong again.

The following factors drive these predictions:

Differential economic losses from water shortages for agricultural versus municipal water users

The high annual cost and risk of BDCP water

Given the size of commitments and the inevitable diversity of views, voluntary decision-making will enable the “coalition of the willing” to move forward

The strong headwinds facing more state bonds

For better or for worse, Hydrowonk is on the record. The rest of this year and next year should prove interesting times in the Golden State.